Skip to content

Skip to content

Dear Sir / Madam,

Thank you for giving us the opportunity to not just quote for your business but taking the time to get to know who we are. My name is Derren Joseph and Moores Rowland Asia Pacific is a network of firms with 30 offices in 12 Asian countries.

U.S. Pre immigration planning, is not an exact science. What we typically do with our clients is go over their assets line by line and discuss the US tax implications of their holdings.

Points for discussion as part of the pre immigration planning process include –

- Investments in non US entities – https://htj.tax/us-exposed-owner-of-international

- Trusts – https://htj.tax/pre-immigration-tax-planning-trust

- Insurance policy structures – https://htj.tax/pre-immigration-tax-planning

- Domicile – discussed below

- Gift and Estate taxes – discussed below

What follows below is a technical discussion meant for practitioners but you are free to review it to get a sense for the complexity of the process and why professional support is necessary for those with assets.

Feel free to reach out to us to book a pre immigration planning session on Zoom, today.

Contents

- INTRODUCTION

- RESIDENT TESTS

- General Rules

- The Green Card Test:

- The Substantial Presence Test:

- Special Rules

- Reporting-Annual Statement

- Taxable Year

- Effective Date

- The Final Residency Regulations (the regulations)

- RA Definition

- Closer Connection/ Tax Home Exception

- Days of Presence in the U.S. That are Excluded for Purposes of the SPT

- Residency Time Periods

- Coordination With the IRC 877 Expatriation Income Tax Rules

- Taxable Year

- Coordination With Income Tax Treaties

- Exceptions to keep in mind:

- The first Year Election:

- Special Rules Relevant to the RA v. NRA Determination:

- Taxpayer Residence For U.S. Transfer Tax purpose

- Resident Versus Nonresident Status

- U.S. Residence for U.S. Estate and Gift Tax Purpose

- Immigration Status- Illegal Aliens

- Factors Indicative of Domicile

INTRODUCTION

Section 138, Division A, of H.R. 4170 (the Tax Reform Act of 1984) amends Section 7701 of the Internal Revenue Code of 1954, as amended (“Code”). To include, as new Subsection 7701(b), a definition of resident alien and nonresident alien for Federal income tax purposes.

Earlier proposals relating to such definition had been introduced in the House of Representatives on June 30, 1983, as part of the H.R. 3475 (Section 501), and thereafter as part of the Title IV of H.R. 4170 (Section 451), the Tax Reform Bill of 1953 (which originated from H.R. 3475), and which was ordered reported by the House Ways and Means Committee (the “Committee”) on October 21, 1983. Subsequently, on March 1, 1984, the Committee adopted a committee amendment to H.R. 4170 to offer as a subsequent for the previously reported bill. The substitute for the previously reported bill was designated as H.R. 4170, the Tax Reform Act of the 1984. The Conference Committee completed its work on H.R. 4170 on June 22, 1984, and approval by Congress took place on June 27, 1984. Thereafter, President Reagan signed H.R. 417 into law on July 18, 1984.

Thus, effective for tax years beginning after 1984, objective definitions of the terms – resident aliens (“RAs”) and nonresidents aliens (“NRAs”) for Federal income tax purposes are incorporated into the Code. However, the new definition does not affect the determination of residence for the Federal estate and gift tax purposes. In addition, The Joint Explanatory Statement of the Committee of Conference (the “Joint Statement”) also makes it clear that it is not intended that the definition of RA and NRA affect the determination of whether an estate or trust is a U.S. or foreign estate or trust, “except insofar as that determination itself turns on the resident or nonresident of particular alien individuals.”

RESIDENT TESTS

General Rules

Code Section 7701 (b) sets forth the following two (2) test pursuant to which an alien individual will be considered a RA with respect to any calendar year if he: (i) is a lawful permanent resident of the United States at any time during the calendar year (the “Green Card test”) or (ii) is present in the U.S. for thirtyone (31) days or more during the current calendar year and has been present in the United States for a substantial period of time- one hundred eighty -three (183) days or more during a three (3) year period

weighted toward the present year (the “Substantial Presence Test”).

Pursuant to Section 7701 (b)(1)(A), an alien individual is to be considered a RA for any calendar year, if and only if, he satisfies the requirements of the Green Card Test, the Substantial Presence Test or the First Year Election

The Green Card Test:

A lawful permanent resident is defined as an individual who has the status of having been lawfully accorded the privilege of residing permanently in the United States in the accordance with the immigration laws, and if such status has not been revoked (and has not been administratively or judicially determined to have been abandoned). Thus, a lawfully permanent resident continues to be a resident for income tax purposes until he officially loses or abandons the states as lawful permanent resident.

The Substantial Presence Test:

An alien individual is classified as a RA as to a calendar year (the “current year”) if he is present in the United States for thirty-one (31) or more days in the current year and has been present in the United States for one hundred eighty-three (183) days or more during a three (3) year period, weighted toward the current year. This weighting takes place as follows: an alien is considered a RA during the current year if the sum of the days he is present in the United States during the current year, plus one-third (⅓) of the

days present during the preceding year, plus one-sixth (⅙) of the days present during the second preceding year, equals or exceeds one hundred eighty-three (183) days.

As an illustration of the application of the Substantial Presence Test, a NRA could be present for one hundred twenty-one (121) days on an annual basis over a period of years without being considered a RA. [The one hundred twenty-one (121) day number is not an absolute limit, but the average number of days a NRA can be present in the United States over a period of years without being considered a RA under the Substantial Presence Test].

The closer connection/tax home exception provides that if an alien:

- (i) is present in the United States for fewer than one hundred eighty-three (183) days during the current year, and

- (ii) establishes that he has a “closer connection” with a foreign country and a “tax home” in that country, then he will not be treated as a RA under the Substantial Presence Test for the current year [Section 7701(b)(3)(B)]. The commentary to Section 451 of H.R. 4170 by the House Ways and Means Committee (the “House Commentary”) clarifies somewhat the

interpretation of a United States abode will not automatically prevent an individual from establishing a tax home in a foreign country.” The foregoing could be interpreted to mean

that the maintenance of a dwelling in the United States solely for vacation purposes would not prevent the individual from establishing a tax home in a foreign country. Unfortunately, the House Commentary does not expand on the meaning of the term “abode”.

Significantly, the “closer connection/tax home” exception will not apply with respect to an alien who has not at any time during the current year, an application pending to change has his status to permanent resident or who has taken other affirmative steps to apply for status as a lawful permanent U.S. resident. Therefore, an alien should give careful consideration to his actions before applying for a change in status to permanent resident or taking other affirmative steps to apply for status as a lawful permanent United

States resident.

The exception for exempt individuals provides that under certain circumstances, “foreign governmentrelated individuals”, students and teachers or trainees are defined as exempt individuals and may avoid application of the Substantial Presence Test. However, the application of this exception in the case of students and teachers or trainees is limited to a certain number of years.

In addition, an alien individual who is unable to leave the United States because of a medical condition which arose while the individual was present in the United States is not treated as being present in the United States for purposes of the Substantial Presence Test on any day that such individual was unable to leave the United States because of the medical condition. It should be noted that this is a narrow exception limited to persons who require medical attention after arriving in the United States and are

“unable” to leave the United States.

Although no longer likely relevant due to the passage of time, when Section 7701(b) was enacted, some equitable transitional rules were included as to the Substantial Presence Test. Pre-1985 presence of an alien in the United States who has a NRA under current law at the close of 1984 was not counted in applying the Substantial Presence Test; and pre-1984 presence in the United States of an alien who was a RA under current law at the close of 1984 but was a NRA at the close of 1963 was also not taken into account in applying such test.

Also, a third important transitional rule applied with respect to the Green Card Test. Such rule provided that if an individual was a lawful permanent resident of the United States throughout calendar year 1984 or if he was present in the U.S. at any time during 1984 while he was a lawful permanent resident, then the individual was treated as a RA during 1984 for purposes of the individual’s “first year of residency” and for determining the “residency starting date” for such individual (these concepts are discussed below

in II.B.). Thus, if such an individual meets these criteria, then he will be considered a RA as of January 1, 1985, whether that individual is present in the United States on that date or on a later date during 1985.

Section 770(b)(7) defines presence in the United States as any day that an individual is physically present in the United States for any part of the day. However, if an individual regularly commutes to the U.S. from Canada or Mexico, such individual will not be treated as present in the U.S. on any day during which he so commutes.9

In addition, an individual who is temporarily present in the United States on any day as a regular member of the crew of a foreign vessel engaged in transportation between the United States and a foreign country, or a possession of the United States, shall not be treated as present in the United States on such day unless such individual otherwise engages in any trade or business in the United States on such day.

One of the principal modifications made by the Joint Committee was included, as Section 7701(b)(10) (titled “Coordination with Section 887”). A provision w hereunder, if an alien is a RA for three (3) consecutive years under the new statutory definition (a period defined as the “initial residency period”), and after ceasing to be a RA thereafter period, such alien will be taxed during the intermediate period of non-residency on the same items of income that would be taxed to a U.S. citizen who renounced U.S. citizenship for the principal purpose of avoiding U.S. tax. The Joint Statement provides that this rule will apply regardless of the subjective intent of the alien. The regulations add the requirement that the period of residence for each of the years in the initial residency period includes at least one hundred eightthree (183) days. However, this rule will apply only if the alien’s tax, as determined under Code Section 877(b), exceeds the tax applicable to NRAs under Code Section 871.

Finally, the Joint Statement notes that the residence definition contained is not intended to override treaty obligations of the United States. Therefore, in the event of a conflict, the treaty definition of residence will prevail. However, the Joint Statement also stated that:” …notwithstanding the treatment of the alien as a resident of the other country for treaty purposes, the Conference Agreement will treat the alien as a resident for purposes of the internal tax laws of the United States. For example, if the alien

owns more than fifty percent (50%) of the voting power of a foreign corporation, the foreign corporation will be a controlled foreign corporation”.

Special Rules

Section 7701(b)(2) contains special rules that relate to an alien’s “first year of residency” and “last year of residency” and delineate during what portion of such years the alien will be considered a RA or a NRA. Thus, these rules clarify that in the case of an alien who was aq NRA during the entire preceding calendar year, but who is a RA for the current year (the “first year of residency”), the alien will be considered a RA beginning on the “residency starting date”, which may not necessarily be the beginning of the current year. In the case of an alien who is considered a RA under the Green Card Test, the “residency starting date” is the first day in the calendar year on which the alien is present in the United States while permanent lawful resident of the United States (subject, however, to the third transitional rule discussed in II.A. above); and, in the case of an alien who is considered a RA under the Substantial Presence Test, the “residency starting date” is the first day on which the alien is present in the United States during the

calendar year in which the alien meets such test.

In Addition, for purposes of determining an alien individual’s “residency starting date” in the “first year of residency” and the alien’s “last year of residency”, an exception to the Substantial Presence Test is also provided for certain nominal presence in the United States during the year. Thus, for purposes of an alien individual’s “residency starting date” or” last year of residency” the individual will not be treated as present in the United States during any period not exceeding ten (10) days for which period the individual

establishes that he has both a tax home in a foreign country. And a closer connection to that foreign country than to the United States. In this connection, the Joint Statement states that: “[d]e minims presence before start or after termination of substantial presence will generally be disregarded under the substantial presence test”. Thus, the Joint Statement appears to confirm that this provision was not intended to allow multiple periods of nominal presence in the United States without triggering residences status, but intended to permit, without triggering residence status, brief presence in the United States (for example, for business or to find a house) before the alien moves to the United States.

Similarly, these special rules define, in the case of an alien who is a RA during the current year, but who is NRA for the following year, the alien’s residence status in the “last year of residency.”

With respect to the first year residency, last year of residency and related rules, the House Commentary states that “aliens should not be able to switch back and forth between resident and non-resident status for short periods, and that there should be no gap in the resident status when an alien is a resident for a part of two consecutive years.”

Reporting-Annual Statement

Section 7701(b)(8) and the regulations thereunder provide what individuals claiming the benefit of the “closer connection/tax home”, the “exempt individual”, or the “medical condition” exceptions must file annually to establish the basis for such claims.

Taxable Year

Under Section 7701(b)(9)(A), a taxpayer who has not established a taxable year for any prior period will be taxed on a calendar year basis. However, where an alien is treated as a RA for a calendar year but, after application of the foregoing sentence, he has a taxable year other than a calendar year, then he will be treated as a RA for the portion of his tax year within such calendar year. Section 7701(b)(8)(B).

Effective Date

The amendments to Section 7701 apply to taxable years beginning after December31, 1984.

The Final Residency Regulations (the regulations)

RA Definition

Because lawful permanent resident alien status for immigration purposes (so-called “Green card” status) carries with it automatic RA status thus resulting in the worldwide income taxation and significant disclosure and filing requirements, numerous aliens have abandoned (or wish to abandon) such status. If an alien does not hold a Green Card and does not otherwise constitute a RA under the statutory Substantial Presence Test (the “SPT”), such alien would be a U.S. income tax nonresident alien (“NRA”) subject to a much more favorable and limited U>S> tax regime. Generally, speaking, if an alien without Green Card is physically present in the U.S. for 31 days or more during the current year, and when adding thereto one-third (⅓) and one-sixth (⅙) of the days of presence in the U.S. for the two prior years, the alien will satisfy the SPT if the sum obtained is equal to 183 days or more. Further details and exceptions are outlined in the Letter, but are not addressed herein.

To guide those aliens wishing to abandon the Green Card status, the Regulations provide that abandonment will occur if the alien files enclosing his or her Alien Registration Receipt Card with the INS (now USCIS) or consular office stating therein his or her intent to abandon such status. In addition, the term “United States” which may be relevant when determining the number of days an alien is present in the U.S. for SPT purposes, has been amended to exclude the air space over the United States.

Closer Connection/ Tax Home Exception

For many presumed RAs meeting the SPT (but not actually present in the U.S. for 183 days or more during the taxable year), one of the primary exceptions is the Closer Connection/ Tax Home exception (the “CCTH Exception”). In essence, if the alien can prove that his or her “closer connections “are to a foreign country that constitutes his or her “tax home”, the alien can rebut the SPT/RA presumption. The Regulations clarify that an individual’s tax home will be his or her regular place of abode if such individual is not engaged in a trade or business as that term is used in connection with the deductibility of certain expenses incurred when a U.S. taxpayer is away from home on business. Furthermore, the Regulations permit certain individuals (such as a transient executive) to change his or her tax home and closer connections from one foreign country to another foreign country once within a single calendar year.

Next, a taxpayer’s “closer connections” are based on a facts and circumstances test and the determination thereof is far from clear. The Regulations have been modified to include as the additional factor, the location where the alien conducts business activities (other than those that constitute the individual’s tax home).

Days of Presence in the U.S. That are Excluded for Purposes of the SPT

The Regulations clarify that any given day the alien is physically present in the U.S. is excluded when applying the SPT if on such day, the alien is either an “exempt individual,” physically unable to leave because of a medical condition, in transit between two points outside the U/S., or a commuter. After the Regulations were issued, the statute was amended to also exclude certain days of foreign vessel crew members. An “exempt individual” includes certain foreign governmental related individuals, teachers or

trainees, students, and professional athletes. The specific details relating to these exclusions are found in the Letter. In addition, the Regulations further restrict the availability of certain exclusion opportunities, and any alien planning to rely on any exclusion must carefully consider the Regulations.

In connection with the Medical Condition Exception (the “MC Exception”) which many aliens are likely to rely upon, the Regulations are particularly restrictive. The MC Exception hinges on the involuntary nature of the alien’s stay meaning he or she would leave the U.S., but is unable to do so because of the medical condition. The Regulations provide that if the alien did not intend to leave, he or she is not staying involuntarily in the U.S. (i.e the alien would have been in the U.S. regardless of the medical condition). In

rejecting suggestions from practitioners that this intent test be eliminated, the Service responded that to do so would significantly increase the number of individuals qualifying for the MC Exception and would be contrary to what the Service perceives to be Congressional intent. The Regulations then provide guidance on how aliens may prove intent. One factor, for instance, is whether the individual leaves the U.S. within a reasonable period of time (i.e time to make arrangements to leave) after becoming physically able to leave.

Next, the Service rejected suggestions that the term “pre-existing medical condition” include only medical conditions or problems of which the alien was aware and that required treatment before the alien entered the United States. In other words, it would appear under the Regulations that if an alien had, for example, a heart problem or heart surgery many years earlier, had fully recovered and had no problems since, and was present in the U.S. when a problem relating thereto were to once again arise, the condition would constitute a pre-existing condition not originally arising in the U.S. and would likely have an adverse effect on many aliens having similar facts. In the example in the Regulations, an alien enters the U.S. on a given day and has confirmed travel arrangements to leave on a late date. The Service concludes that if a medical condition were to arise in the interim, the days prior to the confirmed departure date would not qualify because the alien’s intention was to remain in the U.S. for that period in any event

Furthermore, the Regulations liberalize the availability of the commuter exception for aliens from Mexico or Canada who commute to employment in the United States.

Residency Time Periods

In connection with an alien’s residency termination date, which date is important when his or her status converts back to that of an NRA, the Regulations clarify that the alien must also maintain a tax home in he foreign country to which he or she has a closer connection, after the U.S. RA termination. This clarification will also apply to the 10-day de minims presence exception described in the Letter

Next, the Regulations clarify the rules permitting certain qualifying aliens to make a Special First Year Election (the “Special Election”) to be treated as an RA. The Special Election will generally be made in situations where RA status will prove favorable. For instance, the Special Election will permit the alien to generate certain non- U.S. trade or business deductions (e.g., home mortgage interest), that would not otherwise be available to an NRA. It will also permit, where relevant, the filing of a joint return, the use of

the standard deduction and the use of multiple personal exemptions. Of course, any alien considering the Special Election should first carefully compare the U.S. income tax consequences of RA versus NRA taxation to make certain that the benefits resulting therefrom are not outweighed by the worldwide income taxation and global disclosure requirements that accompany RA status.

Coordination With the IRC 877 Expatriation Income Tax Rules

The U.S. tax law has for many years included special provisions which in essence are intended to tax an individual who has expatriated (e.g., given up his or her U.S. citizenship) for tax avoidance purposes in a manner that may be more onerous than that otherwise applicable to a NRA. For instance, under the normal U.S. income tax rules, the gain from the sale of shares in a U.S. corporation which does not otherwise constitute a U.S. real property interest, would be income tax free to an NRA. However, if the NRA had expatriated within a certain 10-year period for tax avoidance purposes (which presumption is difficult to overcome), a special rule would subject such NRA expatriates to U.S. taxation on such gain. This same special expatriation provision is made applicable to aliens who have been RAs for 3 consecutive years (the “initial period”), and who then become NRAs for a period of less than 3 consecutive calendar years, and subsequently become RAs again before the close of the third calendar year beginning after the initial. In response to an objection to the proposed regulation, the Regulations are slightly more liberal in that the expatriation rules are not applied unless the alien was a RA for at least 183 days in each of the 3 consecutive years of the initial period. Also, the Service rejected a suggestion that a tax avoidance motive be a factor during the intervening period and concluded instead that the expatriation provision automatically applies if the above requirements are met.

Taxable Year

The Regulations provide that an alien who has adopted a fiscal year as his or her taxable year in a foreign country prior to the period for which he or she is subject to RA tax may adopt, without requesting a change in accounting period, the calendar year for U.S. income tax purposes.

Coordination With Income Tax Treaties

The Regulations clarify that if an alien is a resident of both U.S. and a foreign country with which U.S. has an income tax treaty (a “Dual Resident Taxpayer”), he or she can elect to compute his or her U.S. income tax either as a NRA or RA; however, such alien will be treated as RA for all other U.S tax purposes. For instance, if U.S. shareholders control a foreign corporation, certain “tainted” income such a corporation may be taxed at the U.S. shareholder level whether or not actual distributions are made. For purposes of

the “control” test, a Dual Resident Taxpayer electing NRA status will be treated as a RA and this can adversely affect other U.S. shareholders. An alien who elects NRA status must compute his tax liability in full as an NRA and may not pick and choose certain benefits under a treaty while picking other RA benefits that may be available under the U.S. tax law. The Service rejected suggestions that an alien should be permitted NRA treatment solely for purposes of applying the treaty provisions under which a benefit is claimed. This conclusion is extremely important for a Dual Resident Taxpayer as many treaties, if the alien elects NRA status for U.S. income tax computational purposes, provide that the other treaty country has the executive right to tax certain sources of income such as income from foreign bank accounts. If such income is not otherwise subject to tax in the Dual Resident Taxpayer’s treaty country of residence, significant income tax savings may result.

Furthermore, the Regulations refer to long-outstanding proposed regulations, which if finalized, would permit Dual Resident Taxpayers electing NRA status to be treated as an RA shareholder of a so-called “S” corporation. This method of taxation permits a flow-through of the corporation’s income or loss directly to the shareholders so as to avoid a corporation income tax. To obtain this benefit, certain elections and procedures will have to be followed which in essence assure the Service that no income tax avoidance will

result.

Next, the Regulations confirm that if an alien claims NRA tax status as a Dual Resident Taxpayer, he or she must file a U.S. income tax return as a NRA on Form 1040NR on or before the date prescribed by law (including extensions). The current instruction to the Form 1040NR should be reviewed as to where said form should be filed. The alien must attach to that return a statement in the form required by the Regulations setting forth therein the heading. “TREATY-BASED RETURN POSITION DISCLOSURE UNDER 310.7701(b)-7(b) AND SECTION 114.” The statement must indicate that the alien is claiming a treaty benefit as a NRA and must include: the facts relied upon to support such position, the nature and approximate amount of income, and the specific treaty provision for which a benefit is being claimed.

Unfortunately, the Regulations clearly states that the filing of a Form 1040NRby a lawful permanent resident (“GreenCard” holder) may affect the determination by the INS (now USCIS) as to whether the individual qualifies to maintain his or her residency permit. Thus, any Dual Resident taxpayer electing to compute his or her U.S. income tax as a NRA may be jeopardizing his or her right to U.S. permanent resident status for immigration purposes.

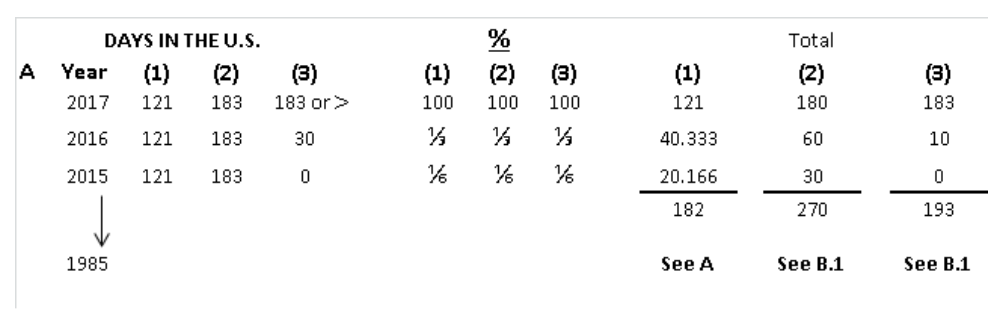

SYNOPSIS OF THE 3-YEAR WEIGHTED AVERAGE SPT FOR RA STATUS

[IF T OBTAINS A GREEN CARD, T WILL BE AN RA BUT D AND G MUST BE CONSIDERED]

Notes: A- The current year being tested for RA vs. NRA. For 2017, T is an NRA in column (1) and (2), but an RA in column (3) as in this Scenario, see B.1 below.

Rule: If taxpayer (“T”) is present in the U.S. at least 31 days or more during the current year and at least 183 days or more under the 3-year weighted average substantial presence test (see % and Total columns above), then “T” is presumed to be an RA subject to the following possible exceptions. Presence in the U.S. includes any part of a day other than regular employment commuter days for Canadians and Mexican, days individuals are in transit from two foreign points and temporary presence days of foreign vessel crew

members.

Exceptions to keep in mind:

- Closer Connection Tax Home Exception- Form 8840. T cannot use this if T, at any time during the current year, has an application pending to change status to that of a Green Card holder or if T is present in the U.S. for 183 or more days in current year. Consider closer connections and tax home

- Exempt Individuals- Form 8843. For foreign government -related individuals, teachers or trainees, students (and immediate family members of all such persons) and some temporary presence of professional athletes.

- Medical Condition Exception- Form 8843. Narrow exception for presence of T unable to leave due to medical condition which arose in the U.S. T cannot rely on pre-existing medical condition.

The first Year Election:

Can help a T who cannot technically meet the 3-year weighted average substantial presence test in the current year and who does not have a Green Card- very specific rules must be met.

Special Rules Relevant to the RA v. NRA Determination:

The Residency Starting Date

The Residency Termination Date

The Nominal Presence Exception

These special rules must be studied in detail so appropriate planning can take place. Failure to do so can

prove very costly.

Taxpayer Residence For U.S. Transfer Tax purpose

Resident Versus Nonresident Status

U.S. Residence for U.S. Estate and Gift Tax Purpose

Preliminary, it should be emphasized that the concept of “residence” for income tax purposes should not be equated with “residence” for estate and gift tax purposes. The objective residence definitions under 7701(b) (and the final regulations thereunder issued on April 24,1992) do not affect the definition of residence for Federal estate and gift tax purposes/ For estate and gift tax purposes, residence in the U.S. requires physical presence in some place in the U.S. and the intention to make that place a fixed and permanent home. Christina de Bourbon Patino, 51-1 USTC 9123 (4th Cir.), aff’g, 13 T.C. 816 (1949). Thereafter, the determination of residence in this context must be made independently from the determination of residence for income tax purposes. Also, as discussed elsewhere in this Chapter, one’s immigration status is not determinative of such person’s U.S. estate and gift tax residence, but is merely a factor in that determination

Because the estate and gift tax regulation i n this area are unclear and inconclusive, the determination of a person’s residence for estate and gift tax purposes constitutes a difficult and subjective factual determination.

Intention and Overt Act

The estate and gift tax regulations defines “residence” in a terms of domicile:

“A “resident” decedent is a decedent who, at the time of his death, had a domicile in the United States …..A person requires a domicile in a place by living there, for even brief period of time, with no definitive present intention of later removing therefrom. Residence without the requisite intention to remain indefinitely will not suffice to constitute domicile, nor will intention to change domicile effect such a change unless accompanied by actual removal.” See Regs. 20.0-1(b)(1) and 25.2501-1(b)

Illustrative Cases

“Domicile” for estate and gift tax purposes is a rather nebulous concept. Thus, although many cases have dealt with the issue, no clear rule has evolved. However, even though

most of such

a. In Fifth Ave. bank of New York, Ex’r., 36 B.T.A. 534 (1937):

The decedent, a U.S. citizen. Was born in New York in 1870. Between 1912 and 1920 she travelled back and forth between the U.S. and France. In March 1920 she returned to France, and lived there until her death in 1932.

The decedent’s purpose for remaining in France was to seek medical advice for her diabetes and to help her cousin who was experiencing marital difficulties. In addition, she had often stated to a cousin that she intended to return to the U.S. when she regained her health and her cousin’s problems were resolved. Whenever she renewed her passports, she stated her reason to travel abroad to be “temporary residence and travel” but in later renewals she stated her foreign stay to be “indefinite”. She always stated her domicile as the U.S., paid U.S. taxes until her death, and never claimed foreign citizenship.

The Service attempted to classify her as a nonresident decedent for estate tax purposes by arguing that her prolonged stay in France caused her domicile to change. Under the applicable rules at the time of her death, non-resident decedent status would have adversely affected her estate’s right to an exemption and deduction for certain expenses.

The Court, in finding her to be a resident decedent, stated:

“Two facts must exist to effect a change over to a new domicile of choice, both residence in the new place and an intention to make the new residence a permanent home. There must be both the fact and the intent.”

In Estate of Bloch- Sulzberger, 6 T.C.M 1201 (1947):

The decedent, who was born in Switzerland in 18883 and died there in 1941, had stated under oath in various documents and in visas, reentry permits, and tax returns, that he was a U.S. resident. Upon the decedent’s death, the Service attempted to tax him as a U.S. resident. In addition to his dying in Switzerland, the decedent had retained his home and business interest there, and had remained active with Swiss charities and civic organizations.

To the Court, the problem was not whether or not the decedent had obtained various benefits by perjured statements, but whether or not he was a resident for U.S. estate tax purposes. In finding him not to be, the Court stated:

“(a) resident for estate and gift tax purposes….. Is one who at the time of his death had his domicile in the United States. Intention of the person is extremely important. Domicile is the place which he regards as his home, and where he intends to live. His old domicile continues until it appears that he intends to live there no longer but has an intention to make his home henceforth at some other place and to remain there indefinitely.”

Because the decedent died in Switzerland, retained his home and business interest there, and remained active with Swiss charities and civic organizations, the Court concluded that he intended for that country to remain his domicile.

In Estate of Paquette, 46 T.C.M 1400 (1983):

The decedent, a Canadian citizen, was born in Canada in 1897. He operated two retail stores in Montreal. In addition, he owned two houses in Canada, one of which was located near his stores in Montreal. The other house was utilized by the decedent as a country house. Beginning in 1950 and up to the time of his death in 1975, the decedent made yearly vacation trips to Florida, generally during winter months. Thus, the decedent would generally remain in Florida from October through April, returning to Canada for the summer. In 1955, the decedent retired and sold his business. In 1956, the decedent sold his house in Montreal, and in the early part of 1957 he purchased a house in Florida which was furnished with contents of the house he had sold in Montreal.

After 1971, the decedent’s wife became ill and was not able to accompany the decedent when he returned to Canada for the summer. In the fall of 1971, the decedent sold his country house because it required too much work to maintain and he intended to buy a small house or rent an apartment in Montreal. In 1972, the decedent began to experience a series of illnesses and he was hospitalized and treated in Florida. However, he continued to return to Canada to meet with his professional advisors and friends. In 1974, the decedent executed his Last Will and Testament while in Montreal and stated therein that he was a resident of Canada. He returned to Florida in November 1974, and he remained there until he died in January 1975.

In concluding that decedent was domiciled in Canada, the Court stated:

“In addition to his yearly visits to Canada, decedent maintained numerous contact with his country of citizenship which evidenced hisintention to retain his Canadian domicile. Up until the date of his death, he filed income tax returns in Canada, he voted in Canada, and he maintained a valid Canadian driver’s license as well as a valid Canadian passport. In addition, decedent’s automobile was purchased, registered, and insured in Canada, Moreover, it is not without significance that most decedent’s assets, valued at $556,351.76, were located in Canada. He met with Mr. Larouche and Mr. Bourgeois, regularly in Canada concerning his investments. In order to keep his assets liquid, decedent’s portfolio was divided between deposits in Canadian banks and stocks and bonds of between of Canadian corporations. Decedent returns yearly to actively manage his investments. Decedent met at least twice a year with Mr. Larouche at which he personally made decisions of when and where to invest his money. In fact, Mr. Larouche was prohibited from making changes in decedent’s portfolio unless he received personal authorization.

After careful evaluation of all the evidence , including testimony by those who were well acquainted with decedent, we find that decedent never had any intention to establish a United States domicile. Decedent maintained many contacts with his native country, and followed a 25-year old practice of spending winters in Florida. We find that decedent never intended to remain in the United States indefinitely.”

An Estate of Barkat A. Khan, T. C. Memo 1998-22:

The decedent, a Pakistani citizen, had obtained an immigration long-term permanent resident alien green card and a social security number in the part to help preserve certain U.S. subsidies, but the decedent died in Pakistan in 1991 and although the 1986 through 1990 U.S. Individual income Tax Returns for the decedent had incorrectly been filed as non-resident Forms 1040NR, amended Forms 1040 were filed subsequent to decedent’s death. Decedent’s estate was desirous of resident alien domiciliary status (e.g., it wanted to use the larger unified exemption available to an estate of a U.S. citizen or resident alien domiciliary, but not to an estate of a nonresident alien domiciliary) and based its argument largely on decedent and his wife were not resident alien domiciliary of the U.S. at the time of his death and that decedent’s estate was not entitled to the full unified credit or the marital deduction. In a decision which, in the author’s opinion, had numerous factors both for and against resident alien domiciliary status, the court, in finding resident alien domiciliary status, placed significant weight in the decedent’s obtaining a permanent resident alien “green card” plus a re-entry permit when he left the U.S. to return to Pakistan. The case further substantiates the possession of a green card is not conclusive in determining resident alien domiciliary status, although when taking into account all of the facts and circumstances, it can be an adverse factor.

In Estate of Jack, 54 Fed. CI. 590 (2002):

The parties filed cross-motion for summary judgement to determine whether Canadian citizen employed in the U.S. on the date of his death, having been admitted to the U.S. under a non-immigration, temporary professional classification, was legally capable of forming an intent to be domiciled in the U.S. for Federal estate tax purposes. The decedent’s estate argued that the intent to establish domicile by the holder of a temporary professional visa would be in direct violation of the terms of the visa, so that such an intent would be precluded. The Court granted summary judgement to the Service holding that for Federal estate tax purposes, a Canadian citizen employed in the U.S. on the date of his death, who was admitted to the U.S. under non-immigrant, temporary professional classifications, was legally capable of forming an intent to be domiciled in the United States.

Immigration Status- Illegal Aliens

With respect to the impact of immigration status upon residence status for purposes of estate and gift taxation, so long as the individual in fact resides in the U.S. with no definite present intention of leaving [regardless of what “legal ability” or “disability” the immigration law places him under (compare Rev. Rul, 80-363, 1980-2 C.B. 249 with Rev. Rul. 74-364, 1974-2 C.B. 321 revoked by Rev. Rul. 80-363, 1980-2 C.B. 249, which revoked, and which are discussed below)], he has formed the necessary intent to become a

U.S. domiciliary.

In Elkins v. Moreno, 435 U.S. 647 (1978), the U.S. Supreme Court held in a non-tax related decision that under Federal law, a non-immigrant alien holding a G-4 visa has the legal capacity to establish domicile in the U.S. when the Federal law which governs the granting of the visa does not impose restrictions on intent duration of stay. The Supreme Court continued to note that even though permanent immigration would normally occur through immigration channels, non-restricted nonimmigrant aliens could adopt the U.S.as their domicile under certain circumstances.

Following the Elkins decision, the Service issued Rev. Rul. 80-363, above, in which concluded that the decedent therein formed the intent and did in fact reside in the U.S. with no definite present intention of leaving, and was therefore a resident decedent (i.e., domiciled in the U.S.):

“ The Supreme Court of the United States, in Elkins v. Moreno, 35 U.S. 647 (1978), held that, under federal law, a nonimmigrant alien holding a ‘G-4′ visa has the legal capacity to establish domicile within the United States. The Court concluded that when federal law, such as the statute that governs the granting ‘G-4′ visas, did not impose restrictions on intent or duration of stay, Congress intended that, while permanent immigration would normally occur through immigrant channels, non-restricted nonimmigrant aliens could adopt the United States as their domicile under certain circumstances.

The question of domicile depends on whether the decedent had formed the intent to remain in the United States indefinitely. In the present situation, decedent was a resident since, at the time of death, domicile had been established in the United States, and decedent had formed the intent and did, in fact, reside in the United States with no definite, present intention of leaving. This is true notwithstanding that decedent had entered and remained in the United States with a ‘G-4′ visa.” (at 1980-2 C.B. 250).

See also. TAM 8137027 (a National Office Technical Advice Memorandum which further discussed the relevant issues.)

In connection with illegal aliens, un Rev. Rul. 80-209, 1980-2 C.B. 248, the Service concluded that an illegal alien lived in the U.S. for 19 years with his family, had purchased a U.S. residence and had established strong community ties, was domiciled in the U.S. at the time of his death:

“The requirements for acquiring a domicile are (1) legal capacity to do so; (2) physical presence; and (3) a current intention to make a home in the place……

*****

…..Some of the factors used in determining such requisite intention are home ownership. Local community ties and living with one’s family in the claimed domiciled

See Farmer’s loan & Trust Co. v. United States, 60 F.2d 618 (S.D.N.Y. 1983).

In the present case, the fact that the decedent lived in the United States for a long a time with the decedent’s family and that the decedent established strong community ties indicates an absence of any fixed intention of returning to the native country.

*****

…..The facts in the present case thus indicates that the decedent intended to remain in the United States infinitely.” (at 1980-2 C.B. 249)

Factors Indicative of Domicile

As indicated by the illustrative cases above, the factors which are considered in making the determination of whether an alien is resident for U.S. estate and gift taxation must demonstrate a certain degree of permanence in the U.S. on the part of the alien before he is classified as having a U.S, domicile. As expressed by the Court in the Safe Deposit & Trust Co. of Baltimore, 42 B.T.A 145 (1940), rev’d on other grounds, 316 U.S. 56 (1942):

“…..the acquisition of a domicile of choice involves actual physical presence at a dwelling place in another state, coupled with the concurrent intent to make it a home. Intention involves the idea of fixity, of some degree of performance in the new abode, and must be more than the mere intention to acquire a new domicile.”

In the connection with the determination of domicile, some of the most common factors analyzed in the estate and gift tax context are”

- The amount of time spent by the decedent in the U.S., in the other countries, and the frequency of travel both between the U.S. and the other countries and between places abroad. However, a period of extended physical presence in the U.S. alone will not suffice to establish U.S. domicile.

- The size, cost and nature of houses or other dwellings, and whether places were owned or rented by the decedent. In Estate of Fokker, 10 T.C. 1225 (1948). The decedent maintained a large home in New York and a smaller home in Switzerland. The tax Court found the decedent to be ab U.S. domiciliary. The Court compared the size of the houses and their localities, and stressed that the location of the Swiss home (in St. Moritz) constituted a resort, a pleasure oriented community with international appeal.

- The area or locality in which the houses and dwelling places are located. See. Estate of Fokker, above.

- The location of expensive and cherished personal possessions of the decedent. See, Farmer’s Loan & Trust Co. v. U.S., 60 F.2d618 (S.D.N.Y. 1932).

- The area or location of the decedent’s family and close friends. See, Estate of Nienhuys, 17 T.C. 1149 (1952).

- The places where the decedent has maintained and participated in civic leagues, churches, clubs, etc.

- The location of the decedent’s business interest.

- The location of the bulk of the decedent’s assets, and the location of is professional advisors. See, Estate of Paquette above.

- Where did the decedent file tax returns up until his death. See, Estate of Paquette above.

- Declaration of residence or intent made in visa application for reentry permits, will, deeds of gift, trust instruments, letters, and oral statements made by the decedent. For example, in Bank of New York & Trust Co., 21 B.T.A. 197 (1930), the decedent, a U.S. citizen, spent the last 5 years of her life travelling in France, Italy and other countries in Europe. The Court found that she was a U.S. resident, and that she did not have the intention to abandon her U.S. residency while in Europe since her purposes for being there were pleasure and health. The decedent’s declaration and actions indicated that her home was in the U.S. (e,g., when applying for passport renewals she stated that she was abroad only temporarily, and in two trust instruments and a Will executed by her she described herself as a resident of Washington, D.C). See also, Estate of Fokker, above, Frederick Rodiek, 33 B.T.A 1020 (1936),aff’d, 37-1 USTC 9032 (2d Cir.), Estate of Bloch-Sulzberger, above.

- Whether the decedent used traveler’s checks and international credit cards while in the U.S rather than U.S. issued credit cards and local accounts.

- Whether the decedent obtained and used a U.S. driver’s license as opposed to an international one.

- Whether the decedent acquired in his own name (as opposed to renting) an automobile in the U.S.

- Whether the decedent spent holiday periods with his family, and if so, where.

- Whether the decedent brought his family to the U.S.

- Whether the decedent was engaged in political activity such as voting, public, or military service, abroad

- Reasons or motivations for presence of the decedent in the U.S. e.g., health, pleasure, business, war or terrorism in home country or avoidance of political repression or instability in home country.